In many therapeutic areas, especially oncology, physicians have been using early screening tests for decades. Designed to identify the early signs of a disease or condition before any noticeable symptoms develop, early detection tests support timely medical intervention.

In the U.S. alone, early cancer screenings have been credited with preventing 4.75 million deaths (and counting) since 1975. According to the National Cancer Institute, the prevalence of cancer screenings have contributed significantly to a 34% drop in overall cancer mortality from 1991 to 2022.

Unfortunately, the majority of cancers still do not have a recommended screening test. These cancers are usually diagnosed in symptomatic patients, who typically present in later stages of the disease; experts estimate that these diagnoses account for 70% of cancer-related deaths.

New developments in blood-based molecular diagnostics, which use various molecular signals to detect early-stage cancers, are already here—but what about payer coverage?

To better understand how payers are currently managing access for early detection tests, the MMIT Oncology Index team conducted research with commercial payers representing 119 million covered lives. Let’s take a look at the data.

Early Detection Improves Outcomes—But Coverage Gaps Remain

Our research found that 21 of 30 surveyed payers currently cover early detection tests in one or more oncology therapeutic areas. Payers representing more than 63% of U.S. commercial lives provide coverage for colorectal, prostate, and breast cancer screening, which are three of the most routinely ordered tests.

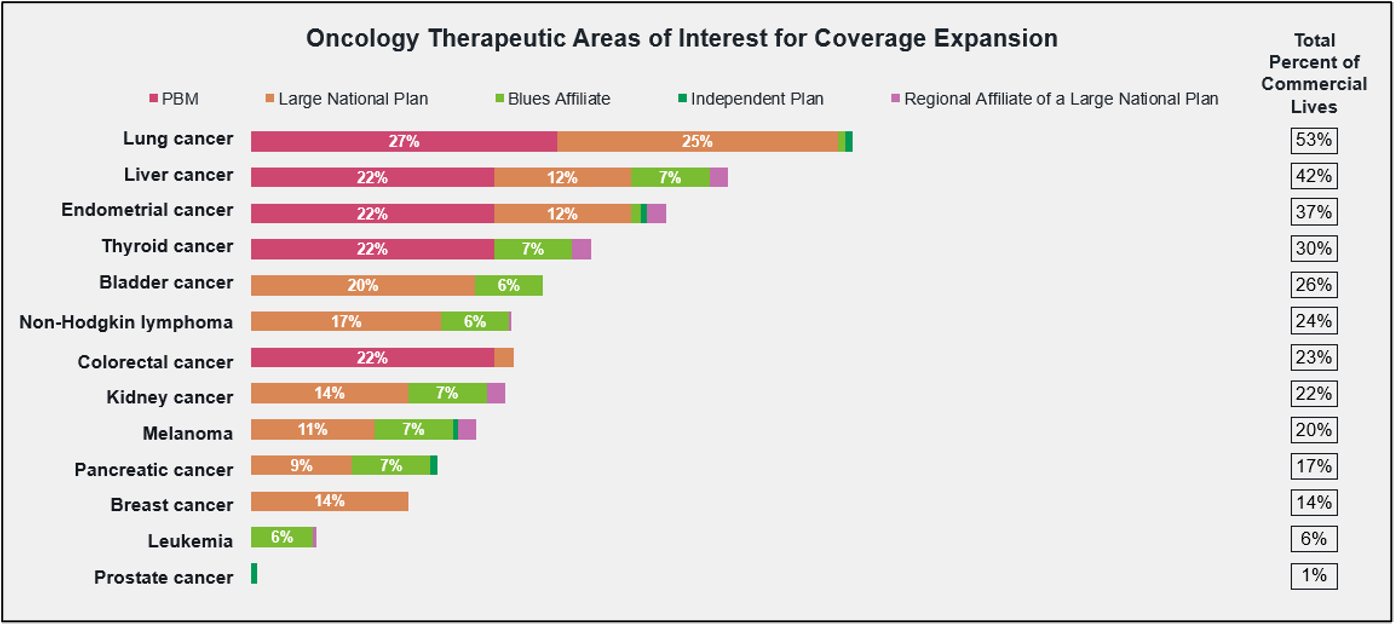

While 45% of U.S. commercial lives are covered for lung cancer screenings, coverage for other early detection tests drops precipitously for less common cancers; for example, early screenings for kidney cancer are covered for only 12% of commercial lives. Interestingly, many payers seem unconvinced of the utility of these screening tests.

Payers who do not currently cover early detection tests indicate insufficient clinical evidence, lack of guideline support, and operational limitations as the primary barriers to offering coverage. As one health plan noted, “They are not part of the NCCN guidelines and effectiveness data is still lacking. We do not discourage members from getting such tests if they are willing to pay for them.”

Fortunately, all payers that currently cover early detection tests are interested in expanding that coverage, with lung, liver, and endometrial cancers most frequently earmarked for future inclusion.

So how do payers decide which early detection tests to cover? According to our research, payers consider clinical efficacy data, the population health impact, and cost effectiveness first and foremost when making coverage decisions. A test’s inclusion in national guidelines, as well as FDA approval, are also decisive factors for most payers.

FDA Approval Remains a Barrier for Multi-Cancer Early Detection Tests

Many oncologists are excited about the recent development of multi-cancer early detection (MCED) tests, which are capable of identifying dozens of early-stage cancers via blood-based liquid biopsies. MCEDs include GRAIL’s Galleri test, which was designated by the FDA as a Breakthrough Device in 2018 and is now in the final stages of Pre-Market Approval, and Abbott’s Cancerguard test.

While these MCEDs are not yet FDA approved or cleared, they are available now with a prescription, with most patients paying out-of-pocket. Payers show limited willingness to cover MCED tests prior to FDA approval. As one payer noted, “Without FDA approval, there is too much uncertainty around the clinical validity and clinical utility of these tests to support coverage. We would need clear evidence that the test accurately identifies cancer, meaningfully improves patient outcomes, and leads to appropriate management rather than unnecessary follow up testing or procedures.”

Once MCED tests receive FDA approval, nearly all payers anticipate offering coverage. The majority indicate a willingness to cover all approved tests rather than just certain ones. If MCED coverage is selective, payers expect to favor tests with stronger clinical performance, clearer utility, and better cost value.

Molecular Diagnostics and AI Expand the Screening Pipeline

Of course, MCEDs are not the only molecular tests in development. Several molecular early detection tests use a single blood draw to detect circulating tumor DNA, while others use methods like analyzing cell-free RNA for tissue-specific cancer signals, or deploying AI-driven molecular sensors to detect enzymes associated with certain tumors. With AI advancements, these tests can support more personalized treatment plans for patients.

According to our research, most payers are at least moderately aware that AI is being used to identify early signs of disease. In the future, payers expect AI-driven early detection tests in various therapeutic areas, most notably Alzheimer’s disease, oncology and neurological disorders. Payers anticipate that the use of AI-enabled tests will have significant impact on earlier diagnosis and treatment initiation, and will also improve diagnostic accuracy.

Early detection testing is entering a pivotal stage of innovation. Although new modalities and methods are in development, payer adoption of even the tried-and-true screenings is still highly variable. While traditional screening tests have established coverage pathways, newer modalities such as MCEDs, AI-enabled diagnostics and precision blood tests must still prove their clinical value (and their ultimate impact on patient outcomes).

For oncology manufacturers—especially those developing therapies for cancers that currently lack recommended screening tools—the rise of new testing innovations presents both a challenge and an opportunity. As new diagnostics expand the ability to identify cancers earlier, manufacturers should begin planning now for the ways in which earlier diagnosis might reshape patient pathways, treatment eligibility and market demand.

Manufacturers can strengthen their position by partnering with diagnostic innovators, supporting clinical evidence generation for underserved tumor types and demonstrating how earlier intervention can improve outcomes and reduce downstream costs. Just as importantly, companies should engage payers early to understand the evidence thresholds for coverage and reimbursement. For manufacturers focused on historically late-stage cancers, aligning treatment strategy with the future of early detection may become a critical competitive advantage.

Learn more about MMIT’s Oncology Index, which offers detailed analysis of payer management strategies and tracks coverage trends, site-of-care preferences, and relationship dynamics.