We are in the midst of a weight-loss drug explosion. Mania for Novo Nordisk’s Wegovy/Ozempic has taken hold of both celebrities and everyday patients, leading to massive shortages and a surge of interest in all glucagon-like peptide 1 (GLP-1) agonists. Industry experts say that obesity has become a top five global market driver, and MMIT’s sister company, Evaluate, estimates the obesity opportunity as exceeding $35 billion by 2028.

The propensity for weight-loss drugs to induce a swell of public enthusiasm is not new. The 1980s brought us the craze for Pfizer’s prescription diet aid Fen-Phen, which was removed from the market in 1997 after studies showed the drug was linked to serious side effects, including cardiac disease. After this removal, there has been a steady stream of prescription medications available to patients looking to lose weight.

Although there are several GLP-1 agonists on the market, there are only three approved so far for weight management. Each has followed the path of its active ingredient being first approved for glycemic control for diabetic patients before adding the indication of weight loss under a different brand name.

In 2014, Novo Nordisk’s Saxenda (liraglutide, first approved in diabetes medication Victoza) was approved for chronic weight management for obese and overweight adults. In 2021, Novo Nordisk’s Wegovy (semaglutide, first approved in diabetes medication Ozempic) was approved to reduce excess body weight and maintain weight reduction for obese and overweight patients.

In 2023, Eli Lilly’s Zepbound (tirzepatide, first approved in diabetes medication Mounjaro) was approved for chronic weight management in overweight or obese adults with at least one weight-related medical condition. And in March 2024, Wegovy became the first weight-loss drug to be approved for lowering the risk of cardiovascular death, heart attack and stroke in obese and overweight adults.

In light of this new indication for Wegovy, let’s take a look at how coverage currently stands, and what these trends tell us about the future of obesity medications in the U.S.

Historic Coverage for Obesity-Specific Treatments

In the past, payers have not been particularly interested in covering weight-loss drugs, despite the fact that numerous conditions have strong links to obesity and can be improved with sustainable weight loss. The reasons for this are numerous, but the overarching rationale has been that obesity has traditionally been considered a lifestyle issue rather than a disease.

In lieu of providing coverage for weight-loss drugs, many payers chose to motivate their members to shed pounds by encouraging healthy lifestyle changes, offering discounted gym memberships, weight-loss programs, and nutritional counseling to facilitate more exercise and better dietary choices.

When payers did choose to provide coverage for obesity medications, they typically restricted utilization by limiting eligibility to only those patients who met certain body mass index (BMI) specifications. They also limited the duration and frequency of medication for weight-loss management, requiring frequent reauthorization.

An Evolution in Payer Perception

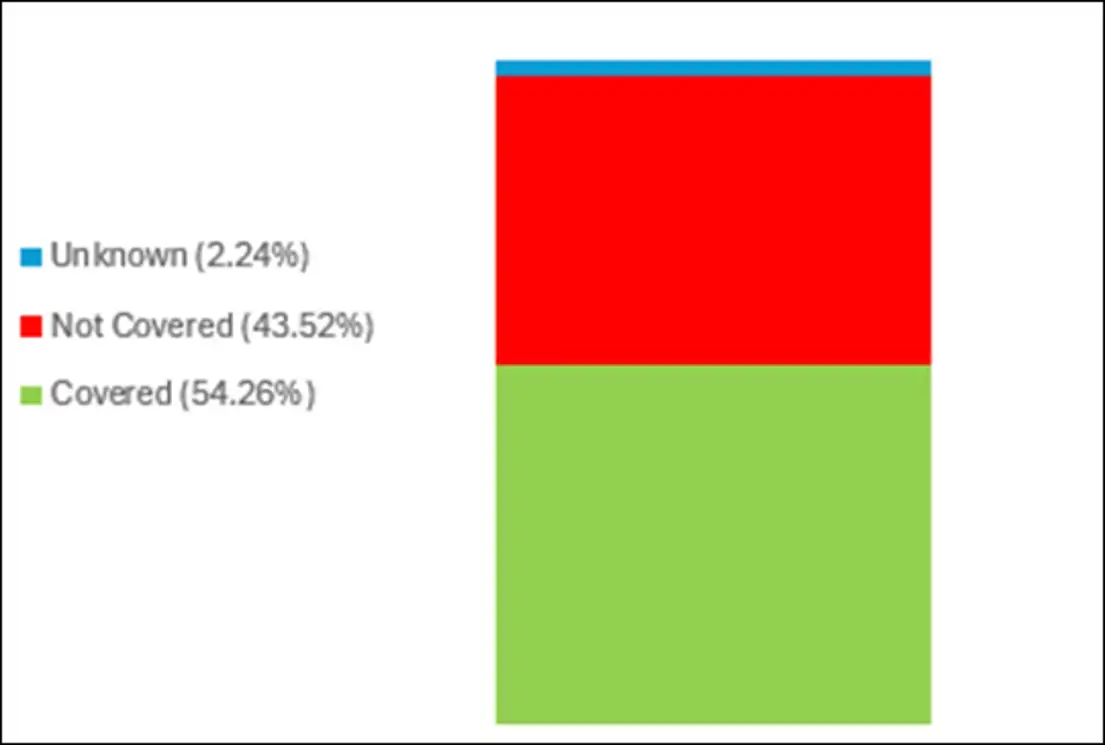

With this new class of weight-loss drugs, payers frequently cite their concerns around the high cost of treatment as an impediment to coverage. Both Wegovy and Zepbound have list prices between $12K to $16K per year. Yet despite these concerns, Wegovy is currently covered at 54% across all channels, according to MMIT’s Analytics policy and restriction data.

What’s driving this change in coverage? Although payers continue to walk the line between lowering costs and improving outcomes, it’s clear that one of the largest impacts of the new craze for weight-loss drugs is the change in how obesity is perceived. Payers are increasingly likely to view obesity as a chronic disease requiring lifelong intervention, rather than a member’s personal failing.

In a recent Payer Message Monitor survey on obesity products, most payers emphasized the wide range of health risks and complications associated with obesity, and many expressed the value of treating value of treating obesity as a chronic disease. In fact, payer behavior in light of Wegovy’s new cardiovascular indication further illustrates the paradigm shift in how the previous distinctions between obesity and other chronic conditions have blurred.

Wegovy’s new indication is clearly prompting payers to re-evaluate their policies. In a recent MMIT poll, payers representing 62% of commercial lives indicated that they were more likely or somewhat more likely to cover Wegovy for their Medicare lines of business based on the newly approved cardiovascular indication. According to Payer Message Monitor insights, the net cost of all weight-loss drugs plays an important role in which product is preferred by a payer. However, most payers in our poll indicated that they were likely to re-evaluate the clinical benefits of each drug in the class in light of Wegovy’s new indication.

Adding momentum to this coverage trend, CMS recently indicated that Medicare Part D plans can add Wegovy to their formularies, and some have already said they will begin covering the weight-loss drug this year. Although commercial coverage is typically more restrictive than government-funded health plans, commercial coverage may well be less restrictive for obesity-related treatments than Medicare or Medicaid, given the pressure of self-funded plans to keep their employees happy and healthy.

Ongoing Payer Concerns for GLP-1 Efficacy and Coverage

Although GLP-1s are an exciting development in the obesity landscape, these therapies are still relatively new and have many unknowns. How long must patients continue to take these therapies to achieve desirable outcomes? What are the typical side effects? Which therapies are best for which patient populations? Continued research will answer many of these questions, but there are already a few considerations payers should keep in mind.

The predominant question for many payers (and patients, for that matter) concerns the sustainability of weight loss. Current research indicates that most patients will need to continue using GLP-1s indefinitely to maintain their weight loss, as changes to a patient’s metabolic baseline do not persist after treatment ceases. An extension analysis of patients from Novo Nordisk’s own STEP1 trial found that “one year after withdrawal of once‐weekly subcutaneous semaglutide 2.4 mg and lifestyle intervention, participants regained two‐thirds of their prior weight loss, with similar changes in cardiometabolic variables.”

If weight rebound is common after cessation of Wegovy and other GLP-1s, payers who cover these drugs may well need to plan for an enormous per-member expenditure for patients who stay on GLP-1s indefinitely. Essentially, this means that payers must be prepared for the long-term costs when deciding member eligibility criteria. Similarly, reauthorization criteria will likely need to be less restrictive to avoid the health risks associated with members re-gaining weight.

To counter this concern, it is entirely possible that the health benefits associated with GLP-1s may outweigh the long-term cost of the therapies. Ongoing research on GLP-1s may demonstrate previously unknown off-target effects. In addition to weight management and cardiovascular disease, potential benefits in stroke, kidney disease, and even depression and addiction may change payers’ entire cost model for their associated members.

Further research and cost-offset models need to be continuously monitored to allow payers to truly understand the impact of these therapies—and update their policies accordingly.

Waiting for a Sustainable Future

Obesity has never been a problem with an easy solution, and there are myriad factors that contribute to an individual becoming overweight. Without tackling the lifestyle and dietary changes necessary to maintain weight loss, patients who stop taking GLP-1s are unlikely to sustain the health improvements they realized during treatment.

As we await the next generation of obesity treatments, which includes oral formulations and combination mechanisms, so much remains unknown about this high-growth market. Will the long-term use of GLP-1s actually lead to reduced costs for payers in treating other comorbid diseases? Could real-world claims data help demonstrate potential cost offsets by reductions in hospitalizations and cessation of other drugs to treat comorbidities?

The increased popularity of weight-loss drugs also brings a number of manufacturing and supply-and-demand questions into play. As payer coverage of weight-loss drugs becomes more widespread, will patients who take similar formulations to treat diabetes face chronic drug shortages? And once we do see more widespread payer coverage, will manufacturers be able keep up with demand?

One thing is clear: payers are no longer dismissing anti-obesity medications as a cosmetic fix, and are instead seeing their full potential. They are more likely to believe that obesity is a chronic disease, deserving of treatment and risk mitigation. This mindset shift toward the medical necessity of obesity treatment is likely to intensify as more weight-loss drugs gain additional indications.

To analyze the pharmacy and medical benefit landscapes, you can rely on data from MMIT’s Analytics solution. For insights into payer and IDN perceptions and behavior, learn more about Message Monitor.