This has been a significant year for the Humira (adalimumab) biosimilar market. AbbVie’s blockbuster drug Humira, an injectable used to treat a range of inflammatory conditions, saw the end of its 20-year, $200 billion monopoly in January. By the beginning of November, nine adalimumab biosimilars had made their market debut.

Pharma manufacturers have been closely following the adalimumab rollout, as this year serves as a case study for biosimilars yet to be approved. At the center of the discussion is a key question for manufacturers with biosimilars in the pipeline, as well as manufacturers of originator therapies: What will have the most influence over payers’ decision-making for biosimilar coverage?

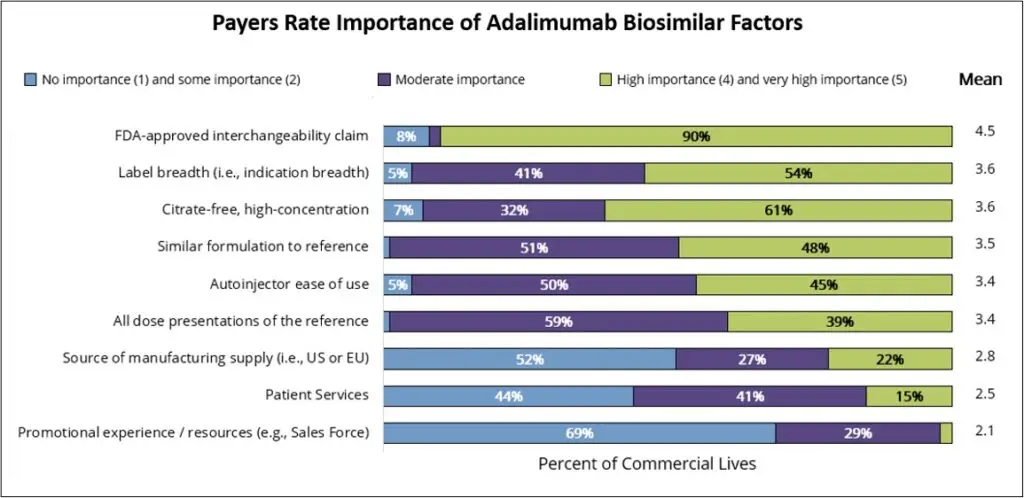

According to MMIT research, payers rank interchangeability and formulation similarity as the two most important factors to consider when determining whether to add an adalimumab biosimilar to formulary—but of course, there are many more factors that play into their final decisions. Let’s take a deeper dive into this year’s biosimilar explosion.

Dual-Pricing and Discounting Strategies

Payers commonly consider a manufacturer’s pricing strategies and likely contract negotiations when deciding on formulary additions. The biosimilar market has taken this a step further, with some manufacturers employing specific dual-pricing strategies with both small and large discounts.

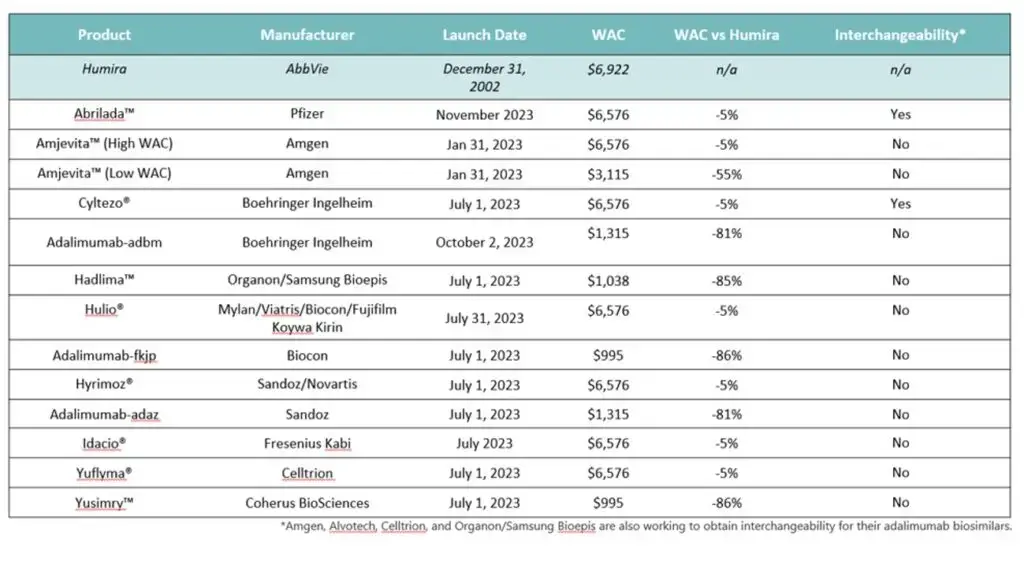

This pricing strategy resembles the commercialization approach taken by Viatris and Biocon Biologics in 2021, when the companies co-launched both a branded and an unbranded interchangeable insulin product. While the branded product (Semglee) debuted at a list price only 5% lower than the reference brand’s wholesale acquisition cost (WAC), the unbranded product (glargine) was 65% lower.

Amgen’s Amjevita, the first Humira biosimilar to market, launched with two different WACs, one 55% below Humira’s WAC and one 5% below. Other manufacturers followed suit, offering differently priced branded and unbranded biosimilars. This approach caters to two audiences. While a significant discount looks better on paper and provides an affordable option for patients, the more expensive pricing allows plans, PBMs and vendors to take advantage of greater rebates.

Other manufacturers, such as Coherus, are offering steep discounts for their branded biosimilar; the company’s Yusimry product launched at an 86% discount. Coherus also collaborated with Mark Cuban’s pharmacy to sell Yusimry directly to patients for even less. Other manufacturers have also deployed deep discounting, as noted in the table below.

Payer and PBM Formulary Selection

So far, payers’ and PBMs’ biosimilar selections have been more or less as expected. Two large PBMs, Express Scripts and OptumRx, selected the same five biosimilars for their primary formularies (both the high- and low-WAC versions of Amjevita, plus Cyltezo, Hyrimoz, and adalimumab-adaz), ensuring that at least one low-priced biosimilar is on their national formularies.

Other PBMs, such as Elevance Health’s CarelonRx, will add Boehringer Ingleheim’s Cyltezo to certain formularies and adalimumab-adbm to its commercial formularies starting December 1, with both offered at parity with Humira. The PBM reasoned that “keeping Humira on our commercial formularies, while adding these biosimilars at parity with Humira, [will] deliver more choice to our members and providers. And by continuing to monitor the pipeline, CarelonRx can support biosimilar adoption while driving competition and increasing access to cost-effective new treatments.”

While some payers are eager to see price competition across the indications that Humira covers, they are expected to initially place the biosimilars on formulary at parity with Humira until they can ensure HCP and patient comfort. This strategy also ensures they do not lose access to the rebates from AbbVie.

Contracting Negotiations and Rebates

Unsurprisingly, contracting negotiations and rebates play a big role in influencing payers’ formulary decision-making for Humira biosimilars. Because of Humira’s dominance for so many years, payers have had to consider whether or not they will keep the branded agent as their preferred drug on formulary or replace it with its biosimilars.

As mentioned, part of this is influenced by pricing. According to a special report by MMIT’s Biologics & Injectables Index team, payers representing ~44 million commercial lives said they would need a biosimilar to be priced 60-75% lower than its branded reference product’s WAC to prefer a biosimilar over the reference product. This applies to five products: BI’s adalimumab-adbm, Organon’s Hadlima, Sandoz’s adalimumab-adaz, Bicon’s adalimumab-fkjp, and Coherus’s Yusimry.

Beyond pricing, payers’ existing contracts with AbbVie also sway the decision to keep or remove Humira as their preferred agent. AbbVie also has two-year deals with several PBMs to secure Humira’s placement on their reimbursement lists, according to Chief Commercial Officer Jeffrey Steward. This may be slowing the adoption of the biosimilars by payers until they review the contracts that are currently in place.

The Weight of Interchangeability

Another important aspect of Humira biosimilars is interchangeability designation, which allows pharmacists to dispense a biosimilar instead of its reference brand without provider authorization. Interchangeability is a meaningful designation for several reasons. For payers, interchangeability can potentially drive meaningful savings, but only if there is high biosimilar utilization. Payers are under pressure to ensure high utilization to account for the loss of rebate dollars from AbbVie.

To the broader market, Humira biosimilars have the promise of reducing prices and drug spending in the U.S. According to calculations from three biosimilar experts published in AJMC, “If every adalimumab biosimilar had an interchangeability designation, the United States could save an additional $765 million annually.” This, again, hinges on a major if.

On the flip side, some experts argue that interchangeability is a nice-to-have perk, but not essential for gaining coverage. To receive this designation, most biosimilars, with the exception of insulin and retinal drugs, are required to go through an additional level of scrutiny via additional switching studies and, in some cases, clinical trials mandated by the FDA.

The significance of the interchangeability designation—and whether this classification is useful to providers making a prescribing decision—is controversial and evolving. In July of this year, the proposed Biosimilar Red Tape Reduction Act was reintroduced to Congress with the purpose of ending the additional layer of scrutiny required for interchangeability. The legislation seeks to “deem biosimilars as interchangeable with their branded equivalent upon their approval by the FDA.”

According to MMIT data, FDA approval and interchangeability claims are seen by payers as most important when considering whether to add an adalimumab biosimilar to their formulary. Payers representing 90% of commercial lives indicate that FDA-approved interchangeability is of high or very high importance. In fact, payers representing 54% of commercial lives noted they would likely exclude a reference product from their formulary when the product’s biosimilars receive interchangeability designation.

More Biosimilars on the Horizon

Beyond dual pricing strategies, contracting/rebate discussions and interchangeability designation, a few additional factors will be important to track in the coming months.

First, the additional launches of Amjevita’s high-concentration formulation and interchangeability designation will be crucial events for this market. The availability of a formulation that provides a more similar dosing experience to Humira could potentially increase utilization for this first-to-market biosimilar.

Another notable event will be payer coverage for Organon and Samsung Bioepis’ Hadlima, which is available in both a citrate-free high concentration and citrate-containing low concentration. The desirability of high-concentration, citrate-free formulations, such as Yusimry’s, is yet another factor to consider. According to MMIT research, 56% of physicians consider this factor to be of high or very high importance when considering whether to prescribe a Humira biosimilar.

The pharmaceutical industry will also be closely attuned to the release of Stelara (ustekinumab) biosimilars, which will make biosimilars available for an additional effective class of anti-inflammatory drugs. In October, the FDA approved Amgen’s Wezlana, the first ustekinumab biosimilar with interchangeability designation. While launch is delayed until 2025, manufacturers will be monitoring the impending launches of multiple Stelara biosimilars in the near future.

As it stands now, the slower adoption of Humira biosimilars on formularies is likely due to several ongoing contracts with AbbVie, as well as continued payer concern about patient biosimilar utilization and the loss of rebate dollars. As contracts with AbbVie come up for renewal at the end of 2023 and beginning of 2024, coverage might change more rapidly.

Manufacturers interested in the best ways to position their originator therapies and/or biosimilars in this crowded market should continue to monitor payer coverage and provider adoption of the Humira biosimilars.

For insights on current and anticipated biosimilar utilization, contracting, and management, learn more about MMIT’s Special Report on Biosimilar Trends.