There is no doubt that payers in the U.S. are investing heavily in AI, but there is much uncertainty about how this technology is currently deployed. While the industry’s AI conversation has focused on generative tools and administrative efficiency, payers are increasingly deploying AI in utilization management, clinical pathways and contracting. According to research from MMIT’s Indices team, nearly half of payers are planning the implementation of at least one additional AI solution in the next 12–18 months.

Although AI-driven changes remain largely invisible to physicians and patients, AI is already beginning to shape how therapies are evaluated, approved and managed. It’s critical for manufacturers to understand the disconnect between payers’ current usage of AI and provider awareness, especially as AI becomes more integrated into payer processes.

As payers use AI to accelerate prior authorization (PA) reviews, optimize treatment pathways and evaluate performance-based agreements, manufacturers will need to rethink how they demonstrate value, support providers, and prepare for increasingly dynamic access controls.

Payers’ Use of AI Remains Largely Invisible to Providers

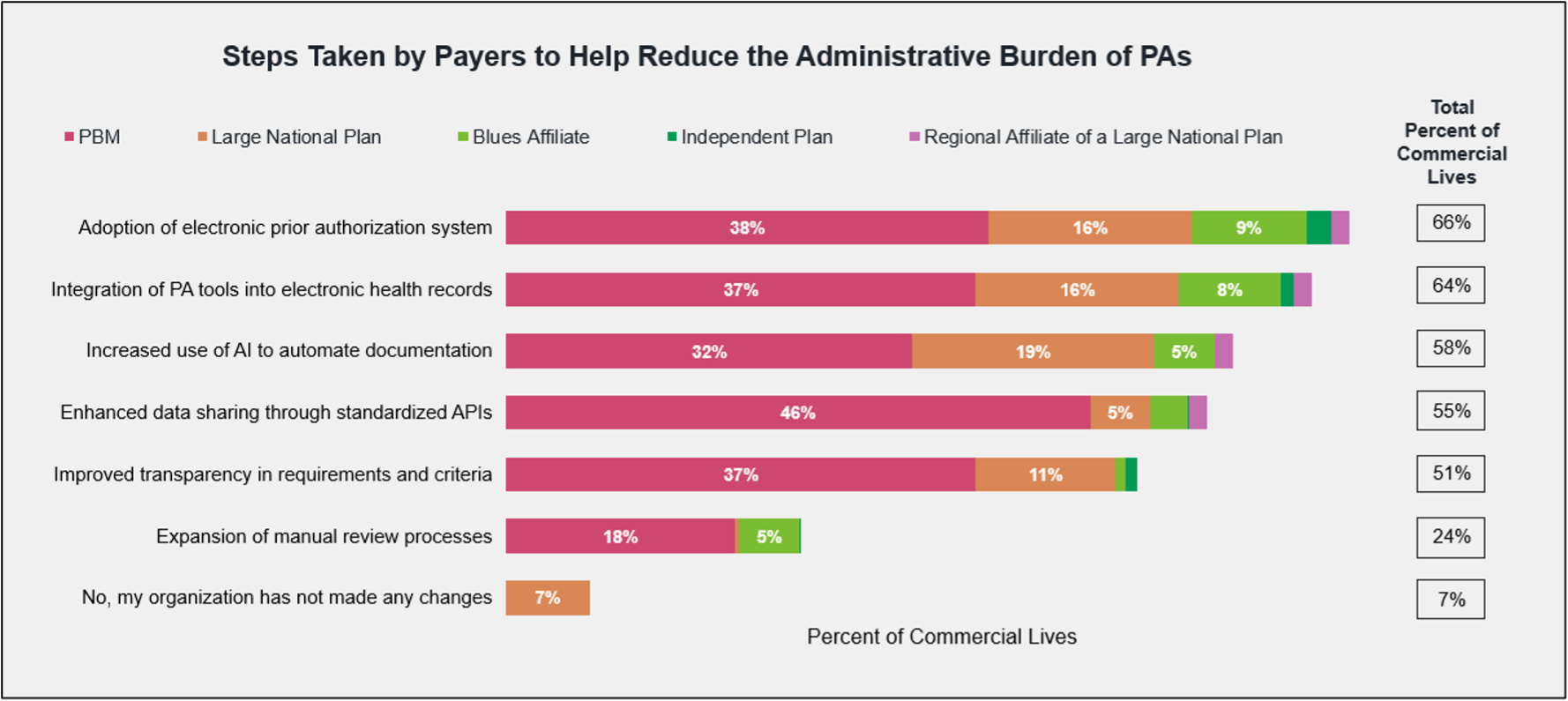

In recent years, payers have taken a variety of steps to help reduce the administrative burden of PAs on providers. The most common steps are adopting electronic PA systems, integrating PA tools in EHR systems, and using AI to automate documentation.

Most providers remain unaware of payers’ use of AI, in large part due to a lack of visible workflow changes. Practice managers, especially those in oncology, are the most likely to have noticed the use of electronic PA systems and EHR integration. However, more than half of surveyed physicians say their practice hasn’t noticed any changes to the PA process at all.

In a more recent survey of payers covering 169.2 commercial and Medicare lives, MMIT researchers found that payers representing 45% of commercial lives are already using AI to automate and streamline parts of the PA process.

Despite this, roughly three-quarters of surveyed physicians, oncologists, and practice managers report that AI has not yet been applied to the PA process. Clearly, manufacturers cannot rely on provider perception to assess the sophistication of payer tools.

How AI Is Starting to Shape Utilization Management

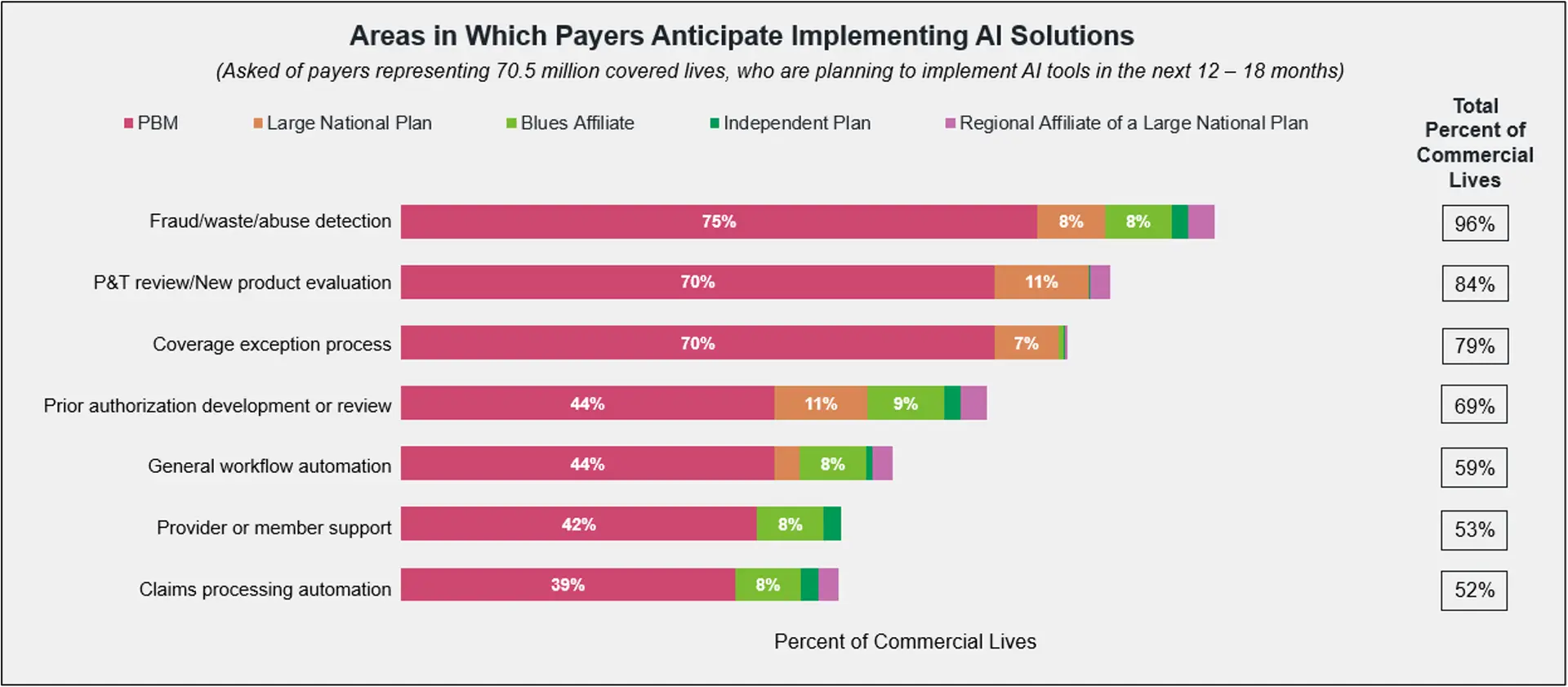

So how are payers using AI thus far? Payers’ most mature AI applications typically include workflow automation and provider/member support, with fewer payers using AI for claims processing automation, coverage exception processing, and early PA automation and review.

Our research indicates that overall, payers are predominantly using AI to standardize, accelerate, and triage decisions—not to replace clinical judgment. This holds true for the PA process as well, at least for now.

Payers report using AI to reduce the administrative workload associated with PAs, most notably by aiding with auto-approvals, clinical rule application, and automated data review. Use cases range from more administrative applications like “reviewing fill history for step therapies” and “reading faxes and incoming data to feed into decision trees” to more sophisticated applications, such as the real-time review of clinical criteria.

As one payer notes, “AI is reducing the burden through automated clinical decision support using natural language processing to help extract criteria details from submissions . . . [and through] provider decision support, which gives real-time guidance at the point of prescribing.”

Most payers are actively preparing for broader AI integration within the next year. Among payers that had not yet implemented AI by the close of 2025, fraud/waste/abuse detection, P&T review and PA review were among the top areas for future adoption, indicating a shift toward risk management and clinical evaluation.

The Next Wave: AI in Clinical Pathways and Contracting Optimization

Payers representing 19% of covered lives already use AI-powered tools to help develop clinical treatment pathways, while payers representing an additional 63% of covered lives are planning for this capability in the future. Similarly, most payers are also planning on using AI tools to support adherence and the optimization of these clinical pathways.

In an Index Access Management Topic Report from March 2026, payers cited enhanced utilization management and provider contracting optimization as the most important cost containment strategies for their organizations in the near future. AI-enabled administrative automation is the top area in which organizations are most likely to increase investment.

AI is also expected to change how payers evaluate and stratify risk in contracting. Payers report only a moderate likelihood of incorporating AI into their rebating and contracting processes within the next 12–24 months, signaling early-stage interest rather than widespread adoption. However, payers representing two-thirds of covered commercial lives agree that AI will definitely influence their contracting strategies in the future.

The few payers who have already use AI in the contracting process cite the ability to track complex clinical endpoints and use predictive pricing in negotiations as key benefits. As one PBM noted, “AI allows us the ability to shift away from rebate-based contracts towards agreements tied to patient outcomes, medication adherence and clinical results.”

What Does This Mean for Manufacturers?

For manufacturers, it’s important to realize that access decisions are likely already influenced by AI-enabled processes, even if HCPs don’t recognize this reality. As the use of AI in the PA process becomes more universal, manufacturers may need to help providers better understand the required documentation and diagnostic sequencing for PAs, in addition to reinforcing accurate coding practices.

Faster, more standardized PA decisions means payers will have even greater reliance on structured data and rules, and less tolerance for incomplete submissions. They will also set a higher bar for clarity and consistency across indications. AI allows payers to apply utilization management rules much more efficiently, which could lead to much faster deployment of new restrictions and expanded step-therapy enforcement, as well as more aggressive utilization management overall. This is particularly relevant for products in crowded therapeutic categories or those without clear differentiation.

Products with clean indication logic, biomarker clarity, and aligned endpoints will be advantaged in the PA process, as AI-driven PA favors clear, objective, and codifiable criteria. The PA process may become more restrictive and algorithmic for therapies with unclear value propositions or inconsistent documentation.

As AI moves into clinical pathway development, manufacturers should be aware that a product’s placement on pathways may increasingly be informed by predictive analytics, sub-population outcomes, and real-world utilization patterns. Instead of relatively static clinical guidance documents, pathways will become more dynamic decision-support systems that are routinely updated to incorporate claims data, real-world evidence, cost trends, provider behavior and outcomes data.

Payer-sponsored clinical pathways are likely to become more operational in nature, tied to larger agreements like value-based care arrangements, site-of-care initiatives, specialty pharmacy routing and the like. As AI-driven pathways evaluate therapies across multiple dimensions at once, manufacturers need to understand that payers are likely to optimize for products that demonstrate the best relative value rather than just the greatest clinical efficacy. Manufacturers need evidence packages that demonstrate not just clinical superiority, but real-world operational and economic value.

In contracting, AI will similarly influence how payers evaluate the success of outcomes- and population-based contracts. Manufacturers will need better longitudinal data strategies and cleaner outcome definitions. Most importantly, they will need to be ready to meet the challenges of payers practicing more sophisticated performance monitoring for these contracts.

The growing use of AI in payer decision-making signals a fundamental shift in how access will be managed in the years ahead. Manufacturers that begin adapting now— by strengthening evidence strategies, improving access support and anticipating AI-driven utilization management trends — will be better positioned as payers move toward a more algorithmic future.

Explore our Oncology Index, Biologics & Injectables Index, and Custom Market Research solutions to learn how unblinded payer perspectives on AI and other trends can help your team.