Biomarker testing is a cornerstone of modern oncology, transforming how clinicians diagnose, stratify, and treat cancer. By identifying particular genetic, molecular, or protein characteristics in a patient’s tumor or blood sample, biomarker tests provide invaluable insights into disease behavior and a patient’s potential response to various therapies.

In recent years, advances in next-generation sequencing (NGS) have dramatically shortened turnaround times without sacrificing accuracy. Rapid NGS tests scan multiple genes at once and can be used with even limited sample material to identify patients with specific biomarkers. They are also much more efficiently processed in smaller batches, which enables oncology providers to conduct in-house testing.

In July 2025, the FDA cleared the Ion Torrent Oncomine Dx Express Test, a rapid NGS companion diagnostic designed to detect guideline-supported biomarkers in solid tumors, including non–small cell lung cancer (NSCLC) and colorectal cancer (CRC). The test is approved for use with both tissue and liquid biopsy samples. However, coverage is not uniform across payers, which can delay patient access to oncology therapies even when testing is recommended or required.

To understand how payers interpret evolving evidence in biomarker testing, MMIT conducted a Rapid Response study powered by the Panel Team. In February 2026, MMIT surveyed 20 payers that cover biomarker testing, in a sample representing large national plans, Blues and regional affiliates, PBMs and independents. Let’s take a look at what the data reveals—and explore how manufacturers can persuade payers to expand testing coverage.

Broad Policy Alignment With National Guidelines

The National Comprehensive Cancer Network (NCCN) recommends molecular profiling in metastatic NSCLC (EGFR, ALK, BRAF, MET, RET) and CRC (KRAS, NRAS, BRAF, HER2, MSI) to guide treatment decisions. For the most part, we found that these evidence-based recommendations for clinical best practices provide a foundation for payer coverage policies.

While payers unanimously cover biomarker testing, the specifics vary by organization. Most payers support both tissue and liquid testing and allow multiple tests per therapy line when there is a clear clinical need. Our research indicates that 40% of payers allow multiple biomarker tests when clinically indicated. An additional 40% cover just one biomarker test per patient, with the ability to retest for disease progression. Only 5% limit coverage to a single test, not repeatable.

Nearly half of surveyed payers believe the first biomarker test should occur before systemic therapy is initiated, while 35% of payers prefer testing to occur at targeted-therapy decision points. A few payers decide on a case-by-case basis when testing should occur. As one payer noted, “We support biomarker testing when it is recommended by FDA labeling and major guidelines, and we time it around when the results are needed to guide treatment selection.”

Regarding the types of biomarker testing preferred by payers, 75% of payers currently cover tissue NGS testing and Polymerase Chain Reaction (PCR) testing, while 70% cover liquid NGS testing and Immunohistochemistry (IHC) testing. A majority also covers florescence in situ hybridization (FISH) testing.

Cost-Efficacy Data is Key to Expanded Liquid NGS Coverage

While most payers (60%) view liquid and tissue NGS as equally reliable, a significant percentage (35%) still favor tissue-based testing due to its longer track record and perception of “higher diagnostic accuracy.”

For payers that already cover liquid NGS, our research indicates that coverage expansion hinges predominantly on strong clinical guideline support, supplemented by economic and real-world evidence to demonstrate the utility and value of these tests. As one large payer noted, “Evidence that liquid NGS is accurate, clinically actionable, guideline-supported, and economically reasonable is what drives coverage decisions.”

Most of these payers (93%) say alignment with NCCN/ASCO/ESMO guidelines is required for them to expand their liquid NGS testing coverage, while 71% of payers report that cost-effectiveness analyses are key. More than half of these payers would also like to see prospective outcomes studies and real-world utilization data to support expanded coverage.

Of the six payers that currently do not cover liquid NGS testing, all cited cost-effectiveness analyses as the key evidentiary factor that might lead to reconsidered coverage, followed by real-world utilization data and national guidelines alignment. Prospective outcomes studies were rated the least influential factor. As one regional affiliate noted, payers are looking for “clinical value drivers around efficacy of testing and the direct/indirect medical cost offsets.”

Rapid NGS Platforms Are Accelerating Payer Reassessment

Our research indicates that FDA clearances of rapid NGS platforms like the Ion Torrent Oncomine Dx Express are influencing payers’ perspectives on biomarker testing. The majority (75%) of surveyed payers reported that they were ‘likely’ to ‘extremely likely’ to update coverage criteria for liquid NGS biomarker tests. Most of these payers (80%) say these updates will occur within a year.

As one large national payer said, “We update our molecular testing policies on a routine cycle, and most of the changes are driven by new FDA cleared diagnostics, stronger guideline recommendations, and better concordance or outcomes data. As liquid based testing continues to mature, we expect more evidence to support broader use, which naturally moves these reviews forward.”

Most payers (80%) indicate that faster turnaround times for biomarker testing are ‘moderately’ to ‘very influential’ on future decisions to cover multiple tests per patient, such as liquid testing followed by tissue-based testing. As one payer explained, “Faster turnaround times directly impact treatment decisions, particularly in oncology where delays can affect first-line therapy selection. If liquid testing provides rapid, reliable results, it increases the clinical justification for allowing multiple tests per patient (e.g., liquid first, tissue to confirm or fill gaps), supporting timely and guideline-aligned care.”

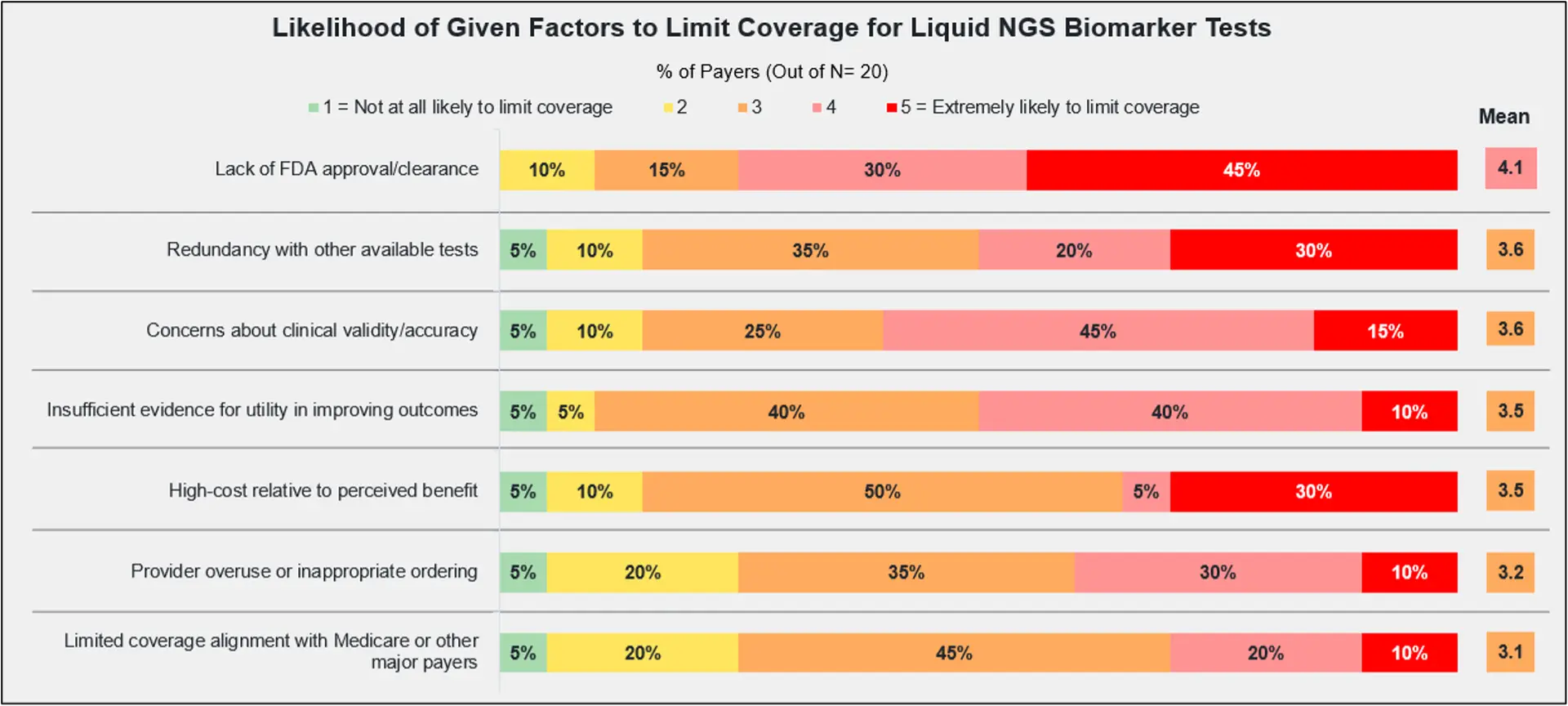

Of course, payers want to see improvements in clinical utility, outcomes, and concordance data before adjusting their policies. Payers ranked the lack of FDA approval as the primary reason to limit their coverage of liquid NGS testing, with ‘redundancy with other available tests’ and ‘concerns about clinical validity/accuracy’ next in line.

These findings show that regulatory endorsement continues to be the strongest driver of payer coverage decisions. Faster turnaround times are attractive to payers, but are not sufficient alone to alter their coverage policies without evidence showing improved patient outcomes.

Payers Require Strong Comparative and Economic Evidence

While molecular testing rates for NSCLC and CRC increased in recent years, studies show that many eligible patients still do not receive all recommended molecular tests. This is in keeping with a retrospective study that found that across all cancer types, less than 50% of patients underwent biomarker testing before first-line treatment, leading missed opportunities for treating patients with targeted therapies—and ultimately, to poorer outcomes.

In light of our research, it seems clear that payers will require strong comparative and economic evidence to expand testing access. These findings underscore the need for manufacturers to align evidence generation with payer decision frameworks. As FDA clearances of rapid NGS tests continue, manufacturers should keep in mind that faster turnaround times may influence payer coverage for multiple tests, but policy expansion depends on measurable clinical outcomes. Payer concerns about the higher cost of liquid NGS tests and diagnostic redundancy remain in place.

To improve patient access to targeted therapies, oncology manufacturers must be proactive in their efforts to combat coverage variability. For wider adoption of liquid NGS, companies should focus on generating robust real-world evidence, comparative studies, and economic models demonstrating patient benefit. This evidence can form the basis for payer policy supporting the use of non-invasive liquid biopsy tests, such as this Blue Cross Blue Shield policy for CRC patients who demonstrate medical necessity.

One payer summarized the evidentiary need in this statement: “We look for strong concordance data, prospective outcomes evidence, and real-world performance that shows the test can reliably guide treatment decisions. It is also very helpful when the test becomes part of an FDA indication or is supported by major guidelines like NCCN, ASCO, or ESMO. Clear comparisons with tissue-based testing, turnaround time improvements, and information on how often the results directly change therapy decisions would also support coverage evaluation.”

Manufacturers can improve payer coverage for liquid NGS testing through:

- Early engagement with payers to clarify their evidence expectations, which can help to accelerate coverage updates and ensure patients have access to precision oncology treatments.

- Cost‑effectiveness analysis (CEA), such as this study that determines an incremental cost-effectiveness ratio (ICER) for NSCLC profiling strategies.

- Outcomes studies, such as this real-world study in NSCLC, which indicates that patients who were enrolled in clinical trials following comprehensive genomic profiling via liquid biopsy experienced better survival rates without increased overall costs.

- Data on liquid and tissue biopsy concordance, such as this study for patients with advanced solid tumors.

As the biomarker landscape evolves, the ability to rapidly validate payer sentiment via custom payer perspective research will give manufacturers a strategic advantage.

For quantitative data and qualitative feedback on coverage decisions, learn more about MMIT’s Rapid Response surveys. For information on current and future access restrictions within specific oncology therapeutic areas, learn more about MMIT’s Oncology Index.