The landscape of patient access has become increasingly complex, intensified by evolving channel dynamics, greater biosimilar investment, and legislative reform. As payers evolve their utilization management tactics, manufacturers must also become more sophisticated in their access strategies.

To explore these topics, MMIT and The Dedham Group conducted the second annual State of Patient Access Survey to collect insights from 250+ pharmaceutical and biotech executives focused on market access and brand strategy. Let’s take a look at a few of our findings.

Cost Pressures and Tighter Controls

Our research indicates that for pharmacy benefit therapies, new-to-market blocks are considered a top access barrier. These policies, which block coverage of a newly approved product until the payer conducts a formulary review, are typically in effect for 6-12 months after FDA approval. According to MMIT Analytics policy and restriction data, the prevalence of new-to-market blocks has been steadily ticking upward over the last few years. As of 2024, 56% of U.S. covered lives are affected by these blocks, which makes it challenging for patients to begin treatment on new therapies.

Two of the most-cited patient access barriers relate to the ongoing shifting of costs toward manufacturers and patients, rather than payers. Manufacturers are specifically concerned about the rebating required to avoid more restrictive payer management—such as step edits beyond the product’s label, or restrictions which cite a trial’s inclusion/exclusion criteria. Manufacturers are also concerned about high out-of-pocket cost for patients. As co-insurance rates increase, patients are paying a greater percentage of a drug’s overall price, which can negatively impact medication adherence.

On the medical benefit side, high out-of-pocket cost was in fact manufacturers’ chief concern, which is unsurprising, considering that there is a greater use of patient co-insurance for medical benefit therapies. Clinically restrictive management was also a top patient access barrier. Although medical benefit products have historically been less managed than their pharmacy benefit counterparts, over time we’ve seen increased reliance on restrictive prior authorization criteria and step edits—not to mention the absence of coverage.

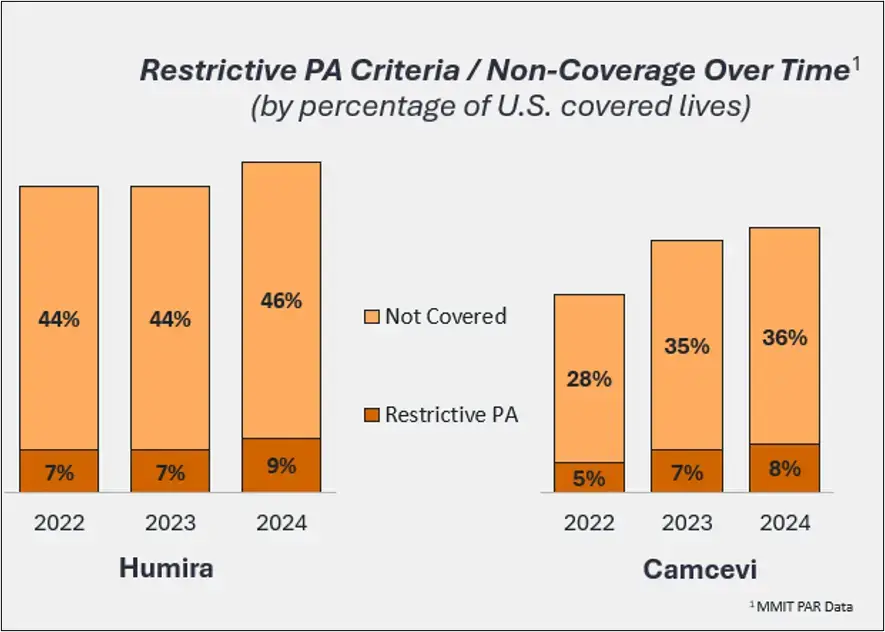

In Figure 1, for example, we see a consistent story of increased restrictions across two drugs from different categories, oncology and immunology. Despite their differences and the fact that one drug is impacted by biosimilars and one isn’t, the trends are similar. This increased stringency in payer management of medical benefit therapies is due in large part to the influx of biosimilars, which we will discuss later on.

Figure 1

For both the medical and pharmacy benefit, manufacturers are also concerned about payer distribution and dispensing management. Site-of-care limitations impact when and where patients can receive treatment, while provisions for white or brown bagging can complicate therapy distribution. The fifth major access concern for manufacturers, regardless of benefit area, is the impact of the IRA and other legislation on access strategy.

Impact of the IRA

The IRA introduced multiple reforms which continue to significantly affect manufacturers, from capping out-of-pocket spending for Medicare enrollees, to Medicare drug price negotiation, to the CPI penalty for raising the price of Medicare drugs faster than inflation.

On average, our survey respondents agreed that the IRA would have at least some impact on anticipated launch pricing, though opinions vary as to the exact scenario. More than one-third (38%) of pharma stakeholders expect that CMS price negotiations will prompt manufacturers to be more conservative with their launch prices, to avoid being selected for price negotiation. However, more than half (52%) of pharma stakeholders expect that IRA will lead to higher launch prices. As there is now a penalty for exceeding price increases past the rate of inflation, manufacturers might front-load these costs in their initial pricing.

While all of the provisions of the IRA are focused on Medicare plans, we were curious about how the IRA will impact future pharma investments. Will manufacturers try to mitigate their Medicare exposure by deprioritizing future drugs in indications with a greater Medicare book of business?

In fact, 76% of pharma stakeholders said that their organizations are deprioritizing product development in therapeutic areas with a high rate of Medicare enrollment, due to the IRA’s provisions. As a result, we could potentially see fewer investments in areas such as high blood pressure, cholesterol, heart disease, arthritis, and even diabetes.

In addition to the impact on pricing and investment, the IRA is also influencing reimbursement. CMS is attempting to drive more access and adoption to biosimilars with an enhanced physician reimbursement rate for qualifying biosimilars, which are now paid at the reference product’s ASP +8%.

The Imminent Explosion of Biosimilars

Since the first biosimilar was approved in 2015, biosimilars have had a growing impact on market dynamics. These effects will undoubtedly intensify between now and 2030. Over the next five years, 88 biologics are facing a loss of exclusivity, representing an estimated market of $100+ billion. To understand the significance of the coming tidal wave of biosimilars, let’s take a closer look at the market opportunity.

As of Q1 2025, 73 biosimilars have been approved by the FDA for 20 different biologic reference products, although not all of them launched immediately following their approval dates. Of these 20 biologics, 10 had at least one biosimilar available throughout 2024. According to Evaluate data, biosimilars captured 47% of the market share for their originator biologics last year—which represents an estimated $10 billion in sales.

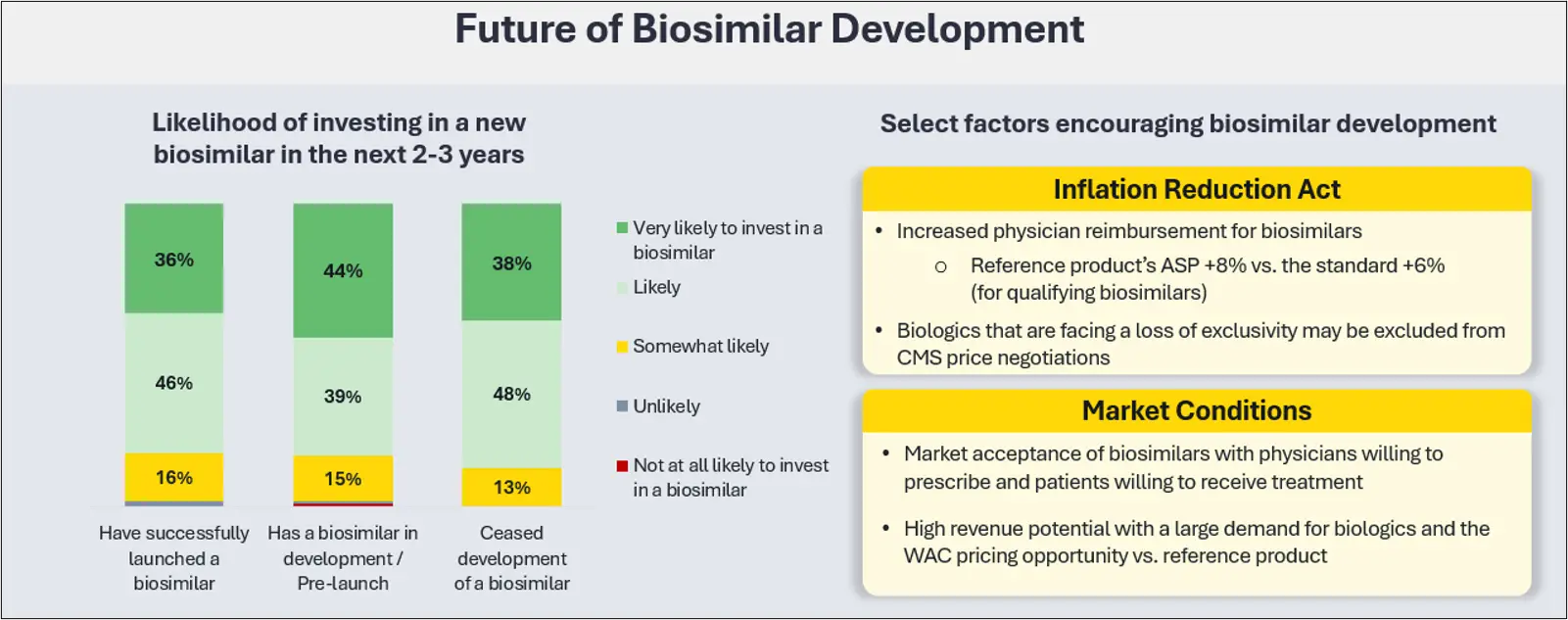

Given the market share potential, our 2025 State of Patient Access survey sought to understand the draw of biosimilar development for pharma companies. After segmenting manufacturers by their previous and current biosimilar experience, we found that the vast majority (82% and above) of manufacturers in each category are likely or very likely to continue their investment (Figure 2).

Past failures did not always preclude pharma companies from considering future biosimilar development. With so many blockbuster agents—including Eliquis, Keytruda, Opdivo, and Darzalex—facing loss of exclusivity soon, manufacturers will have ample opportunity to develop and launch a competitive biosimilar.

Figure 2

Our survey indicated the patient access landscape and navigating pricing pressures are the key to successful biosimilar launches. If a manufacturer determines that a new biosimilar agent may experience significant access roadblocks—whether those be payer restrictions, HCO barriers, or patient affordability issues—they may stop exploring the investment in favor of an opportunity with more preferential access.

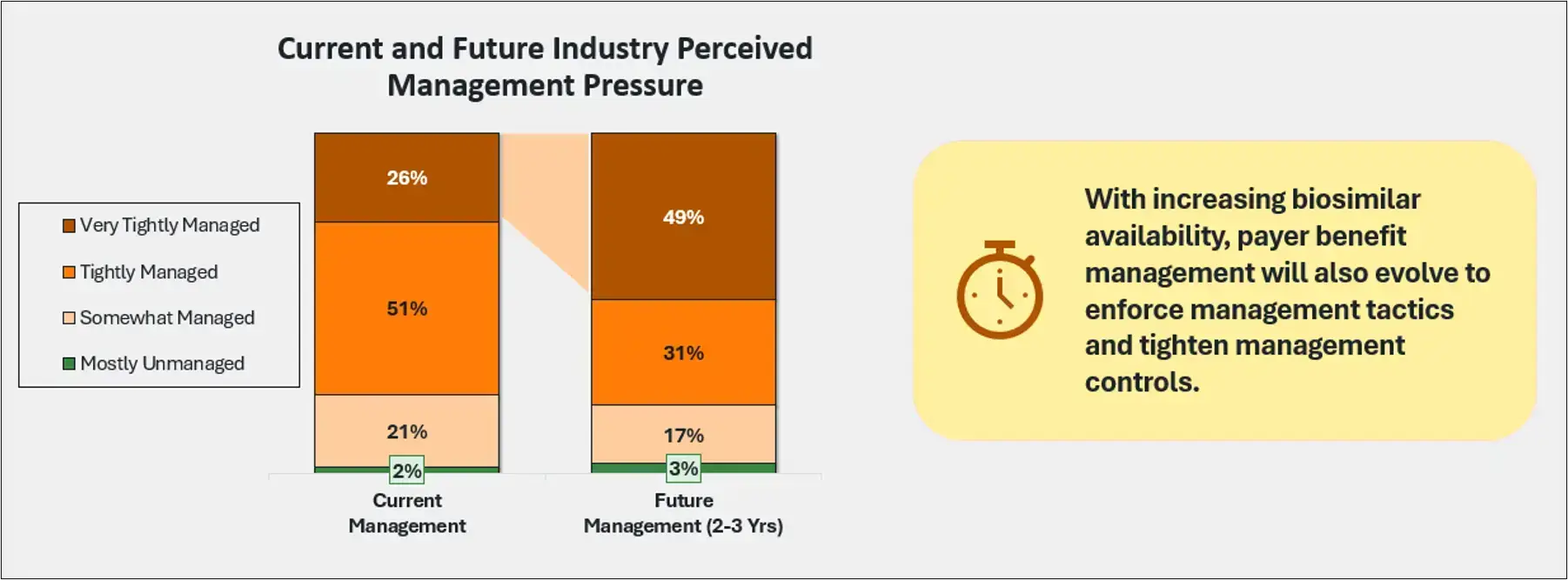

Overall, the evolution of biosimilars is intensifying access pressures and driving more competitive pricing. As more biosimilars become available and/or receive interchangeability status, providers will be more willing to use them, which will bolster payers’ ability to implement preferencing. This increased biosimilar adoption—along with the vertical integration we’re seeing in the market—means that payers will have greater control and ability to pull through utilization management tactics.

Figure 3

In our survey, pharma stakeholders reported that they expect tighter formulary management and increased step edits in the near future (Figure 3). Even with increasing biosimilar availability, originator products will still be on the market. In addition to more restrictive payer management, we expect to see increased rebating and contracting, which will have a significant impact on ASP erosion and overall pricing economics.

As the landscape evolves, pharma companies and biotechs are continuing to shift their market access planning earlier in the development lifecycle. Almost one-third (29%) of survey respondents are beginning market access planning in Phase I, while half (50%) are fully engaged in market access planning in Phases II-III. Essentially, pharma companies are evaluating access earlier on to make informed decisions about the viability of pipeline products.

To hear more results from our primary research, join us on May 14 for a webinar, hosted by BioPharma Dive: The State of Patient Access: Maximizing Access Strategies in the Era of Biosimilars.