Copay accumulator and maximizer programs are now firmly embedded in the commercial market, and their influence on patient access and manufacturer strategy is becoming impossible to overlook. In the first installment of our two-part series on copay accumulators and maximizers, we shared recent Indices research on how payers are deploying and measuring these programs.

In this follow-up blog post, we look at the downstream effects of copay adjustment programs and suggest a few strategies for manufacturers trying to protect patient access and ensure the sustainability of their patient assistance programs (PAPs).

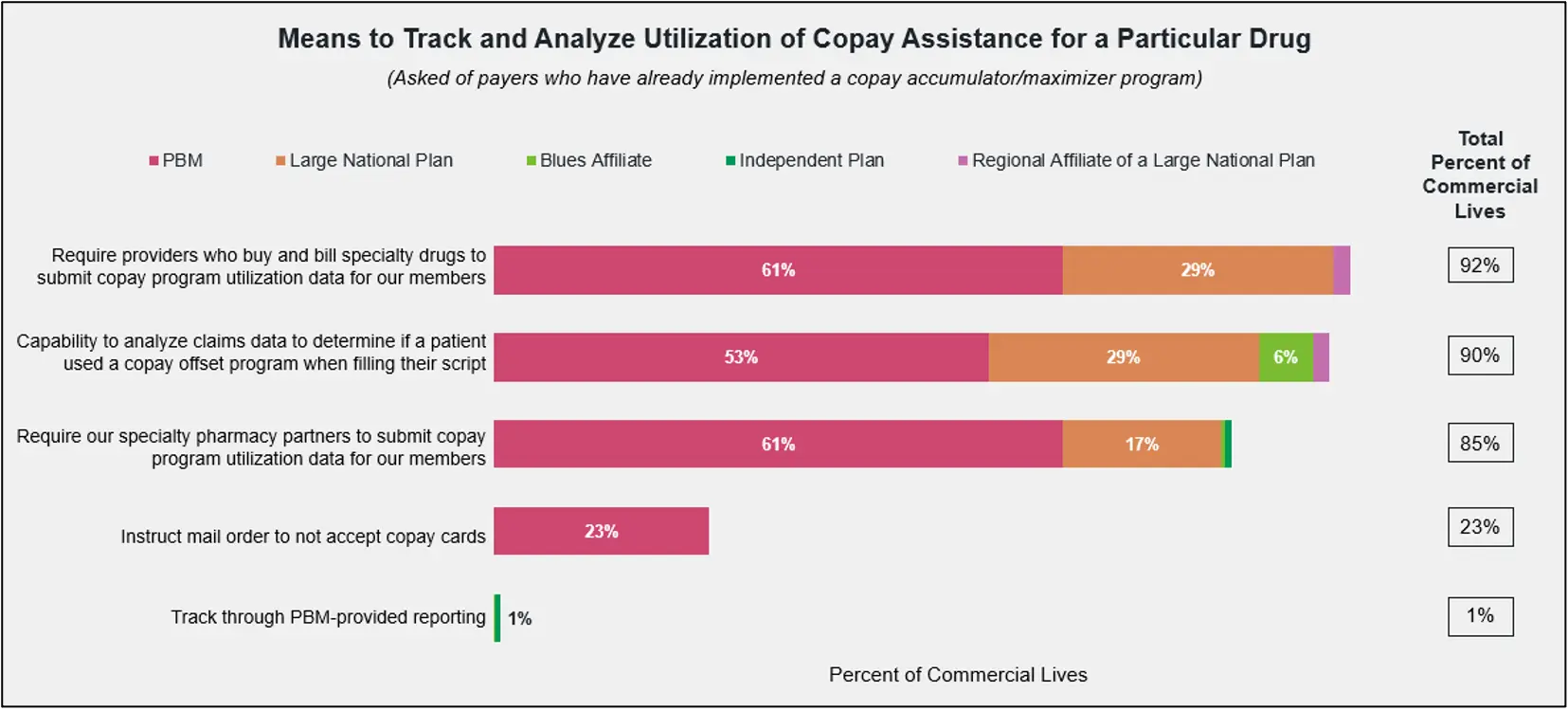

Copay Programs Are Financially Appealing for Plan Sponsors

On average, payers estimate that more than half of plan sponsors have opted into their copay accumulator or maximizer programs. Projected plan sponsor adoption rates for copay programs show little change from current averages, indicating steady participation rather than expansion.

Surveyed payers estimate that almost half of their members—46% and 48%, respectively—are currently enrolled in a copay accumulator or copay maximizer program. Member enrollment in copay adjustment programs is expected to increase by nearly 10% during the next plan cycle.

Payers representing 80% of commercial lives say their plan sponsors have the flexibility to offer both accumulator and maximizer programs simultaneously, enabling broader cost-control strategies.

Specialty Drugs with PAPs Are Prime Targets for Copay Programs

When asked how their organization decides which drugs are eligible for a copay adjustment program, payers said their main targets are specialty drugs with significant manufacturer assistance and a high budgetary impact. Eligibility for copay maximizer programs centers on the existence of manufacturer copay assistance, with one payer commenting that their PBM targets “any drug where a PAP is available.”

As one payer reported, “We use a third-party vendor that maintains a list of medications targeted for copay max (>200 drugs targeted).” Another payer said their organization “looks at the value of the copay card, potential savings to the plan over a 12-month period, potential member savings, the ability of our preferred pharmacies to operationalize the program for a particular drug, and our revenue.”

Our research indicates that few payers independently determine drug inclusion in copay programs. Most defer to plan sponsors or collaborate with them, highlighting the shared decision-making dynamic in benefit design. In general, sponsors prioritize overall drug cost, prevalence of copay assistance, and therapeutic category spend when deciding which drugs to include.

Savings Flow Primarily to Plan Sponsors, Not Patients

Most payers (representing 84% of commercial lives) report that plan sponsors receive savings when members are enrolled in copay programs, reinforcing the financial incentive for adoption.

Plan sponsors typically receive savings through premium discounts, shared savings models, and full pass-through arrangements. As one payer explained, “The program is funded through a shared savings arrangement, where 25% of savings are retained to offset the cost of program administration.”

Most payers (representing 65% of commercial lives) acknowledge that savings from copay program enrollment rarely reach members directly. When they do, it’s typically through premium reductions or indirect benefits tied to lower overall healthcare costs. As one Blues affiliate noted, “The members do not save unless they are able to have the funds cover their entire year of therapy.”

Regulatory Pressure Prompts Mixed Payer Responses

Despite the savings they deliver for plans and PBMs, most payers acknowledge that copay adjustment programs rarely benefit patients. In our research, payers representing 78% of commercial lives at least somewhat agreed that these programs “prevent patients from accessing the care they need.” Even more agreed that they have a negative impact on medication adherence and can expose patients to higher costs.

Payer ambivalence about copay adjustment programs is reflected in how they respond to new state bans. Payers representing 56% of commercial lives say they have responded to regulatory changes by simply reverting members to traditional benefit designs. Almost half of payers indicate that they have responded by lobbying at the state or federal level to preserve such programs, while one-third of payers say they have negotiated with manufacturers in response to a new ban—a dynamic that may signal future opportunities for collaboration.

Manufacturers Strive to Protect Access and PAP Funding

Indeed, many manufacturers are already fighting back against copay adjustment programs. Payers representing 72% of commercial lives say manufacturers are strengthening their partnerships with specialty pharmacies, while payers representing 55% of commercial lives note that manufacturers are shifting support to the medical benefit when feasible. One-third of payers report that manufacturers are also creating alternative patient assistance programs to sidestep adjustment programs.

As state-level regulation continues to expand and CMS signals future scrutiny of copay adjustment programs, manufacturers should prepare for a landscape in which:

- Payer behaviors diverge across states, requiring more nuanced, geography-specific engagement strategies.

- Benefit designs continue to shift toward maximizer-type models, even though they might be labeled differently.

- Collaboration with specialty pharmacies and third-party partners is essential to ensure PAP dollars are applied as intended.

- Evidence of patient harm (such as non-adherence, abandonment, or delayed care) carries increasing weight with regulators and policymakers.

If they can advocate for policies that align PAP use with clinical intent, manufacturers have a real opportunity to directly influence benefit design conversations. The next phase of market evolution will likely reward pharma companies that take a more assertive, data-driven approach to protecting both patient affordability and the sustainability of their PAP investments.

Learn more about MMIT’s Biologics and Injectables Index and Oncology Index, which provides unblinded payer responses on access management topics like copay adjustment programs, as well as TA-specific deep dives and custom research.