When the Inflation Reduction Act (IRA) first passed in late 2022, payers rushed to respond. On paper, the bill’s intentions were clear: this legislation sought to lower drug costs, reduce patients’ out‑of‑pocket burden, and empower Medicare to negotiate prices for the first time. In practice, however, the ripple effects have been far more complex for manufacturers, prescribers, and payers.

Roughly three years later, payers are now reassessing their strategies for navigating this shifting landscape and determining what changes to make for 2026 and beyond. Let’s take a look at our most recent payer research for insights into their calibrations.

Early IRA Response: Compliance First, Strategy Second

Immediately after the IRA passed, payers’ primary focus was compliance. Payers made educated guesses about how to respond based on anticipated shifts in utilization patterns and the expected impact of CMS negotiations, manufacturers’ pricing changes, and rebate dynamics.

The restructuring of the Medicare Part D benefit capped patients’ out-of-pocket (OOP) Medicare prescription drug costs at $2,000 per year, which impacted millions of beneficiaries. In March 2023, payers surveyed for MMIT’s Special Report on the IRA believed that the $2,000 OOP cap would increase the utilization of high-cost specialty drugs by an average of 54%.

In response to this concern, payers implemented strategic imperatives like tightening their formularies and excluding non-negotiated drugs. They expanded utilization management across high‑cost categories, increasing the use of prior authorizations and step therapies, and shifted drugs to different tiers (re‑tiering). They engaged in aggressive rebate optimization, redesigning benefit structures and cost‑sharing models. And in preparation for the Medicare Prescription Payment Plan (MPPP), which allows beneficiaries to spread out their payments, payers also increased their monitoring, appeals, and compliance infrastructure.

Yet according to MMIT Indices research from Q2 2025, only 20% of surveyed payers said their IRA-related strategic initiatives had been ‘highly successful’. Most payers have found the need to adjust their initial approach, with many focusing on revising their formulary management and contracting strategies.

Manufacturers’ Behavioral Shifts Forced Payers to Recalibrate

Of course, payers weren’t the only ones making educated guesses with limited data. Manufacturers also changed their behavior after the IRA, which had an immediate downstream effect on payers.

Because the IRA penalizes price increases that outpace the rate of inflation, manufacturers began launching drugs at higher list prices to preserve their margins over the product’s lifecycle. In turn, these high prices pushed payers to negotiate harder to secure deeper rebates and better guarantees to keep costs in check.

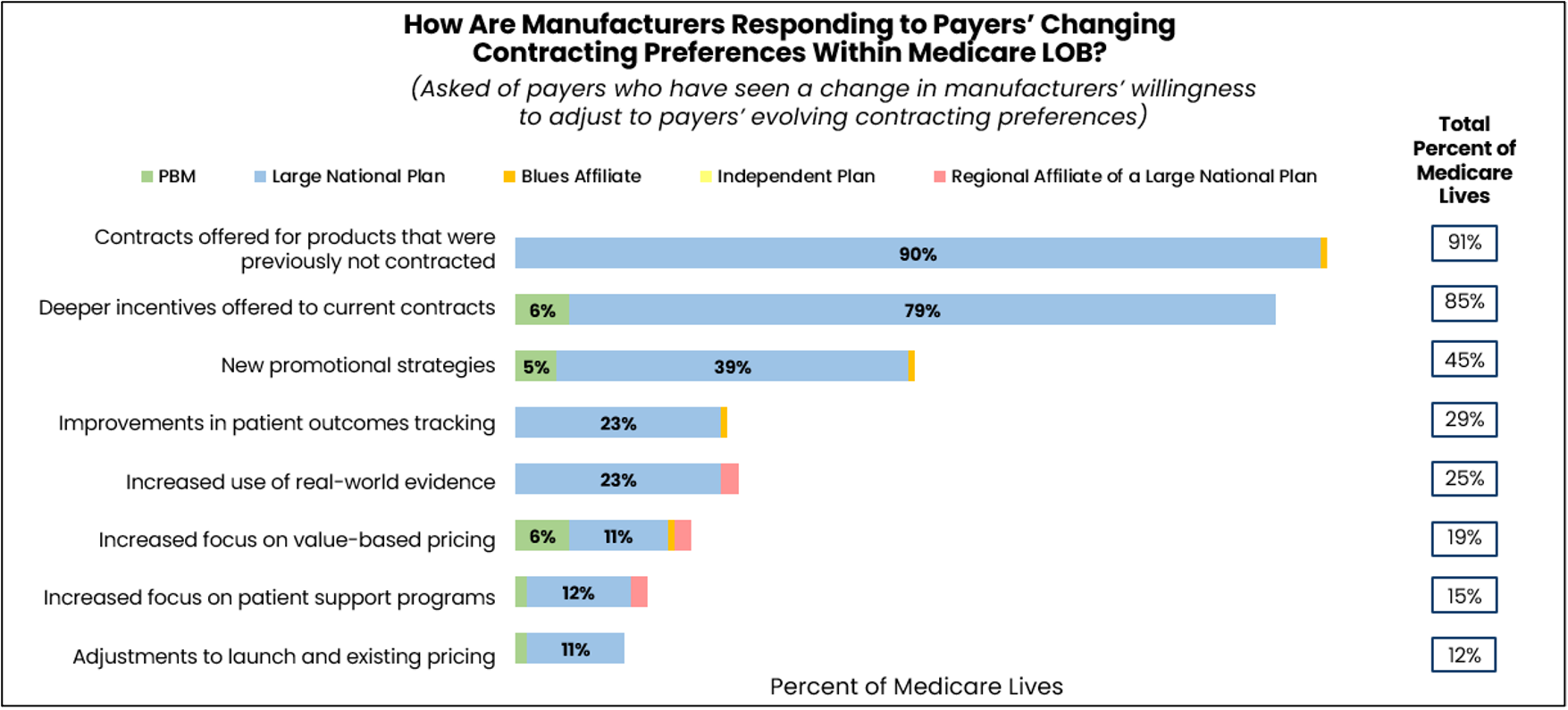

Simultaneously, manufacturers became more open to contracting. Many manufacturers offered rebates on products that had never been under contract before, while others offered much deeper incentives. Some also offered multi-drug portfolio contracting deals.

For payers, the shift created new opportunities, but also forced them back to the negotiation table far sooner than expected. Instead of waiting for their usual contract cycles, many payers re-opened negotiations earlier than planned to adjust terms, secure discounts, and protect budgets.

Real-World Consequences of the IRA for Patients and Providers

Clearly, while the IRA’s intent was to improve patient access and affordability, many unintended real-world consequences have also emerged for providers and patients, including:

- Delayed Access to New Medicines: The IRA’s timeline for price-setting starts at first FDA approval, which has created an incentive for manufacturers to delay the launch of new drugs until multiple disease indications are ready at once. For patients, this could mean longer waits to access novel treatments, particularly for rare diseases and smaller populations where there is less commercial urgency.

- Reduced Incentives for New Indications: With the government able to select drugs for price negotiation just seven years after launch, there’s less incentive for manufacturers to invest in additional research and clinical trials for expanding approved uses. This could mean fewer diseases see new treatment options added in the years following a drug’s initial approval.

- Limited Evidence for Clinical Guidelines: The push for rapid price negotiation may reduce the time and resources spent collecting post-approval evidence. Providers could have less data to guide clinical decision-making for new therapies.

These downstream effects underscore the complexity of drug pricing reform. As manufacturers recalibrate their strategies and payers intensify negotiations, the true impact on patient access, treatment innovation, and the evidence base for care will continue to evolve.

Payers Prepare for Uptick in Utilization, Expected Losses

Although the $2,000 cap on OOP spending was expected to drive significant utilization spikes for high-cost drugs, our research indicates that Medicare payers are split on whether this has actually occurred.

As of June 2025, payers representing 46% of Medicare covered lives said their organization had not witnessed a shift in the utilization of high-cost prescription drugs. Of the payers who had not yet seen a utilization shift, however, more than half expected to see one by the end of 2025.

Along with the potential greater use of expensive specialty therapies, payers are also concerned about inefficiencies like wastage. As one payer noted, “The cap is easily achieved when a patient is on a biologic, a high-cost medication, or a GLP-1. Once a patient has hit the cap, we expect to see increased wastage and refills since the patient will pay $0 for the remainder of the year.”

Payers representing 48% of Medicare covered lives say the OOP cap and the MPPP are very or extremely likely to boost Medicare patients’ willingness to pay for higher cost therapies. One payer said, “With lower out-of-pocket costs and the option to spread payments over time, patients are more likely to consider therapies they may have avoided before due to cost.”

For most payers, the implementation of the OOP cap and MPPP has had no impact on the level of restrictiveness of their Medicare formularies. As of Q2 2025, however, 38% of surveyed payers said these IRA changes have led to restrictions in their Medicare formularies. These payers are using tactics like increased prior authorization, more step therapy and redesigned tier structures to manage their formularies.

As one payer says, “Low-tiered drugs had to tier up to make up for the already high-tiered drugs that are now being dispensed at discounted out-of-pocket pricing.” Some payers are moving from flat co-pays to co-insurance on some tiers, while other plans are limiting the number of preferred agents, favoring drugs that provide value across multiple indications.

As one health plan explained, “With the $2,000 out-of-pocket cap, Medicare beneficiaries pay less, and MCOs like my company must absorb a much larger percentage of the cost, especially in the catastrophic phase. There has been, as a result, a tightening in utilization controls, with the addition of step edits or prior authorizations specifically in high-cost therapeutic areas.”

Intensification of Therapeutic Area Targeting

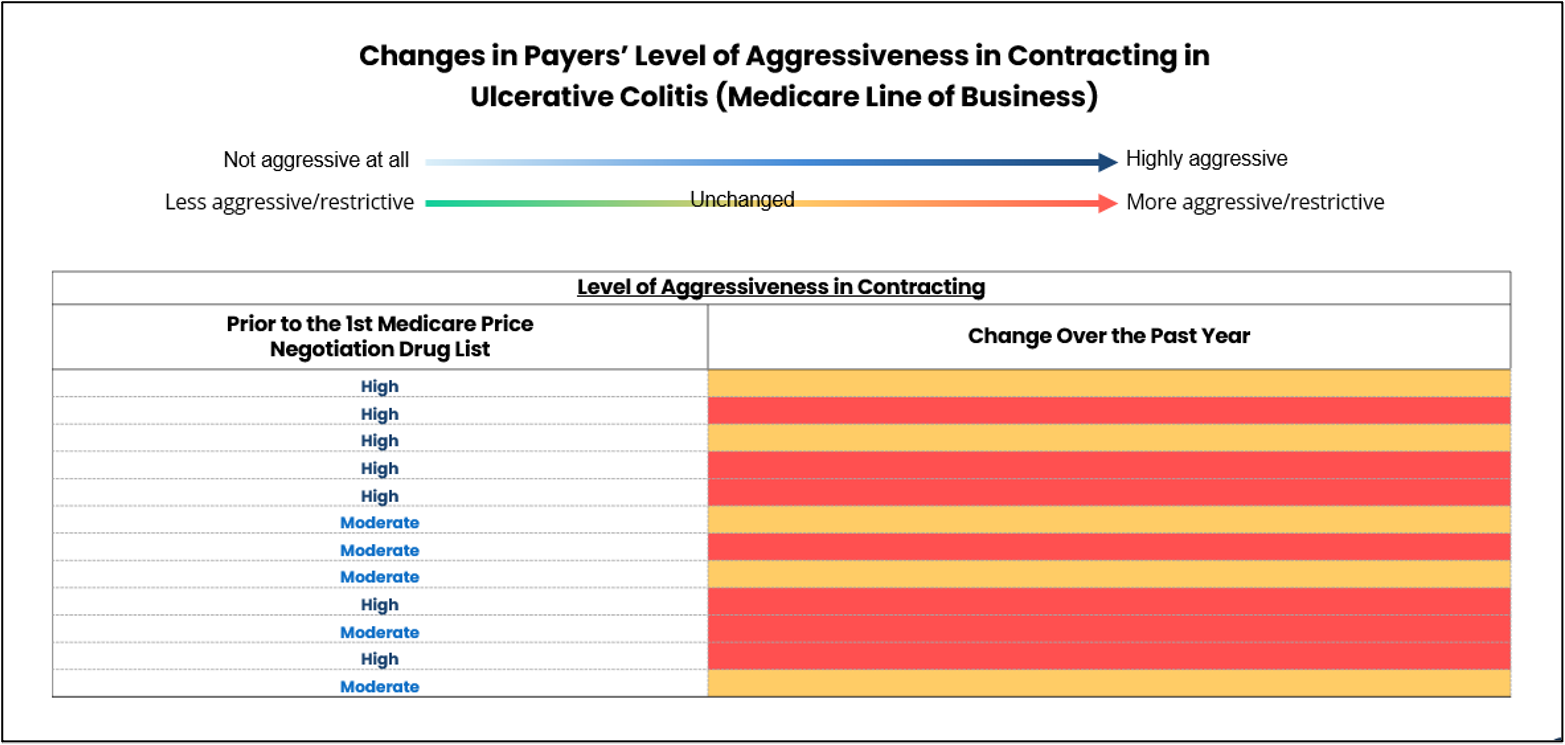

In August 2023, CMS announced the first list of drugs eligible for the Medicare Drug Price Negotiation Program (MDPNP). Before that moment, payers were most aggressive in their contracting for specific high-cost therapeutic areas (TAs) like diabetes, rheumatoid arthritis, and ulcerative colitis.

After the implementation of the IRA, these same categories became even more financially sensitive, due in large part to the $2,000 OOP cap and changes in catastrophic-phase responsibilities. Rheumatoid arthritis and ulcerative colitis drugs, for example, push patients past the OOP cap almost immediately, meaning payers bear most of the year’s cost.

Many of these high-cost therapies were also strong candidates for the MDPNP’s first and second negotiation cycles, further elevating their budget impact. As a result, payers doubled down on these high‑spend TAs, applying even greater intensity through deeper rebate demands and tighter prior authorization.

Before the IRA, payers representing 85% to 91% of covered Medicare lives considered their contracting to be aggressive or “extremely aggressive” in these three areas. Yet in the past year, payers representing 46% to 50% of covered Medicare lives say their contracting has become even more aggressive in those three TAs, as well as in Crohn’s disease. For the other TAs, payers report that contracting has mostly remained the same over the past year.

It remains to be seen if this trend will hold true for subsequent CMS list releases. The second round of drugs eligible for the MDPNP was released in January 2025. By June, payers representing 76% of Medicare covered lives had begun seeking Medicare contracts for drugs that fall within the same TAs that were not included in the list.

In January 2026, CMS announced the 15 drugs selected for the third round of Medicare price negotiations, which will take place this year. For the first time, this list includes not only Part D drugs, but also Medicare Part B drugs; six of these therapies are commonly administered as infusions or injections in a doctor’s office or specialty clinic. The list includes therapies to treat HIV, autoimmune conditions, COPD, cardiovascular disease and several different types of cancer. A negotiated maximum fair price (MFP) will take effect for these therapies in 2028.

What This Means for 2026 and Beyond

When the IRA was first passed, payers were initially concerned with compliance. They met new requirements and prepared for worst‑case scenarios with incomplete information. Now, after weathering the implementation of several IRA provisions and analyzing the real-world data, payers are finally in a position to strategize.

With additional drugs entering negotiation cycles and plan liability increasing under the redesigned Part D benefit, payers will need even tighter control over high‑cost areas. Payers are preparing for:

- Much tighter management of expensive specialty drugs

- Increased reliance on biosimilars

- More strategic contracting with multi‑year horizons

- Higher investments in analytics, real-world evidence, and actuarial modeling

- Earlier pipeline surveillance for high‑impact therapies

Many payers noted that the lessons they’ve learned thus far are helping them refine contracting and improve their forecasting accuracy for 2026 and beyond. According to one payer, all its IRA learnings to date will be “factored into the bid and formulary/UM design strategies, all of which are aimed at reducing medical/pharmacy costs and preserving margin to ensure our Medicare plans remain viable.”

As payer IRA strategies move from experimentation to execution, manufacturers should expect less flexibility around traditional contracting approaches. Payers are increasingly using the redesigned Part D benefit and Medicare negotiation timelines to push for earlier engagement, broader leverage across therapeutic areas, and more durable financial protections. One-year rebate deals are giving way to multi-year agreements, portfolio-based arrangements, and guarantees tied to utilization, net cost exposure, or budget predictability—particularly in high-spend categories and TAs facing biosimilar pressure.

For commercial and market access teams, this means earlier pipeline surveillance and tighter alignment between clinical and contracting strategies. Success in 2026 will depend on anticipating where payer pressure will intensify and entering negotiations with greater flexibility about how contracts are structured.

Pharma companies will need to present a clear plan on how they can help payers manage long-term risk. Manufacturers that align early pipeline planning, contracting strategy, and value narratives around these realities will be better positioned to sustain access in an increasingly constrained Medicare environment.

For insights into general access management trends like payer response to the IRA, learn more about MMIT’s Biologics and Injectables Index and Oncology Index, which also provide TA-specific deep dives and custom payer research.