Over the past decade, health systems have seen a rapid influx of private equity, with a six-fold increase in acquisitions totaling $10 trillion. As private equity firms continue to explore new methods of investment in health care, the recent announcement that Walgreens Boots Alliance will be acquired by Sycamore Partners seems to be a natural progression in strategy.

What does the introduction of private equity into one of the largest pharmacy chains in the U.S. mean for the industry? While this kind of investment is new for retail pharmacy, a review of the impact of private equity on health systems offers a glimpse into what we can expect with a Walgreens acquisition.

Lessons Learned from Health System Acquisitions

Studies on this topic have identified several possible pathways the Walgreens acquisition may follow. Potentially, the acquisition could inject fresh ideas and new methods of thinking into an organization which has been in business since 1901. Additionally, the influx of new cash into Walgreens’ business operations may expedite its development of innovative programs and efficiencies, as it will no longer be bound to stockholder perceptions.

Research indicates that the introduction of private equity in healthcare creates concerns for payers. While some studies suggest that patient outcomes remain the same after a private equity acquisition, others have found that these acquisitions negatively impact patient care. One investigation concluded that private equity acquisition was associated with a 25% increase in hospital-acquired conditions, despite a reduction in surgical volume.

Overall, the negative impacts associated with private equity takeovers include increased surgical site infections, bloodstream infections from central lines, and readmission rates for acute medical conditions. Most concerningly for payers is the potential for direct cost increases, a shift which has occurred in health systems acquired by private equity.

The Clinical and Financial Impacts of Equity Leadership

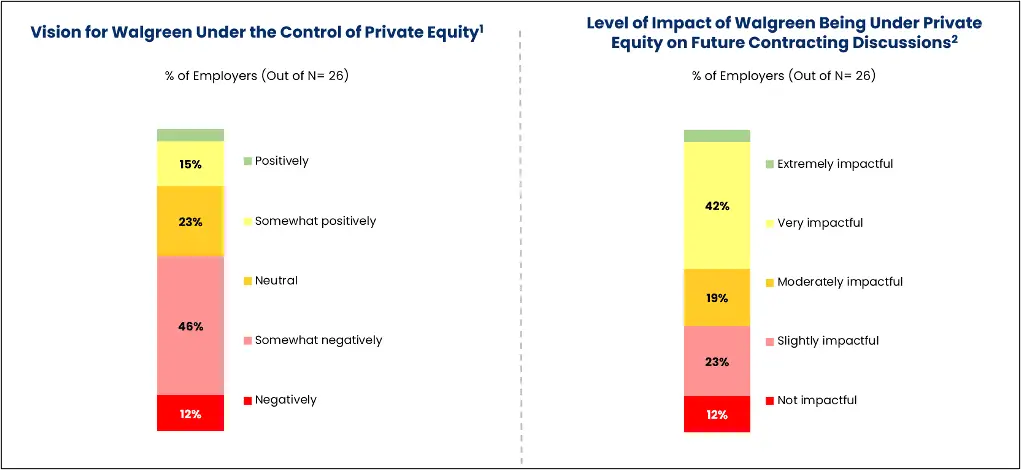

To better understand payer perceptions about the Walgreens acquisition, our team asked 26 payer respondents to share their thoughts. The majority (60%) of respondents viewed the acquisition negatively, and 46% considered the acquisition to be very or extremely impactful on future contracting discussions.

Most payers suggested there may be concerns with retaining Walgreens in their network, especially given the historical context of equity acquisitions decreasing care quality, reducing locations, and adopting more aggressive contracting. As one PBM noted, “There could be contractual issues relative to participant noise and widening of contracting network providers due to poor service levels.”

Most respondents have significant concerns about the potential for an increased focus on profit, whether through an increase in fees or the cutting of staff and/or services. As one regional affiliate said, “I am concerned that private equity leadership will pivot Walgreens’ focus and priorities onto short-term financial gain as opposed to supporting a longer runway mission of quality and safety.” A large national payer concurred, predicting a “decrease in quality. Less of a clinical focus. More of a focus on maintaining the bottom line.”

What makes a retail pharmacy acquisition by private equity unique? To start with, consider the risk to the deep ties between U.S. retail and specialty pharmacies. While the market has trended toward integrating these dispensing pathways, it is possible that a private equity firm might be so focused on profitability that it decides to shed less profitable business components. As private equity companies are not bound by the traditional constraint of stockholder expectations, they may veer in an unexpected business direction at any time.

More Aggressive Contracting Predicted

Traditionally, PBMs contract with pharmacies primarily around drug costs, as well as which pharmacies are included in their network. Large pharmacy chains like Walgreens have a lot of leverage due to the sheer number of locations across the U.S.

Surveyed payers are concerned that this acquisition will lead to a lack of transparency that impedes their negotiations with Walgreens. Understanding a pharmacy’s business approach is critical for contracting, as payers will remain focused on ensuring that care quality does not suffer and patients have sufficient access to care. Walgreens may seek to further reduce its footprint due to underperforming locations, which would lead to a change in strategy.

Payers now expect Walgreens to take a more aggressive contracting approach, focusing on administrative fees and overall patient access, when it enters contracting negotiations for the first time as an equity-run organization. Payers’ previous experience with equity-acquired health systems is that their leadership is often willing to walk away from a contract if they feel they cannot extract enough financial value from it.

Ongoing Tensions Between Payers and Pharmacies

Overall, our research indicates that the acquisition of Walgreens by Sycamore Partners has generated more concern than enthusiasm from payers. With organizations and plan sponsors growing ever more sensitive to cost containment, the introduction of a new variable into a core pillar of the healthcare system will likely lead to a shift in strategies and priorities that may ultimately affect patients’ quality of care and overall access to services.

The impact of this acquisition may result in a profound shift in the dynamics between payers and pharmacies. Manufacturers will need to work closely with both entities to fully understand the changing dynamics between them, and to facilitate informed and productive conversations with key stakeholders.

To better understand these shifting dynamics, consider our Custom Market Research. For payer/IDN answers to your specific business questions, learn about our Rapid Response solution.